Why older homes keep triggering insurance red flags

Older homes promise character, craftsmanship, and often a better price per square foot, but they are increasingly colliding with a harsher reality in the insurance market. Carriers are tightening their standards, flagging aging systems and subtle maintenance issues as reasons to hike premiums, demand repairs, or walk away entirely. If you own or are eyeing a prewar bungalow or mid‑century ranch, you are stepping into a world where charm and risk are now judged line by line on an inspection report.

To understand why your place keeps tripping alarms, you have to see your home the way an underwriter does: as a bundle of probabilities tied to age, condition, and cost to rebuild. Older properties tend to have more things that can go wrong, and when they do, the repair bill is often higher than on a newer tract house. That combination is what keeps triggering insurance red flags, and it is reshaping how you need to maintain, document, and even renovate an older home.

Age, condition, and the new risk calculus

From an insurer’s perspective, the age of your home is not just a number, it is a proxy for how likely something is to fail and how expensive it will be to fix. As homes get older, materials wear out, building standards change, and hidden issues accumulate behind walls and under floors, which is why guidance on home insurance stresses that older structures present unique challenges. When your place no longer lines up with modern safety expectations, carriers see a higher chance of claims and a higher payout when those claims arrive.

That logic shows up in how companies price and structure coverage. Explanations of why age and point out that older materials are more likely to fail and more expensive to replace, so premiums rise to match the risk. Another breakdown of how home age notes that wear and tear increases the likelihood of claims, which is exactly what underwriters are paid to anticipate. In practical terms, that means your century‑old house can cost more to insure than a larger but newer property down the street, even if both would sell for the same price.

Why older homes are harder to insure at all

Beyond higher prices, you are also more likely to run into flat refusals when a home crosses certain age thresholds. Explanations of why insuring older emphasize that carriers are constantly weighing the probability and severity of a loss, and older properties, by their nature, tend to score higher on both. If a fire or storm hits a house built with plaster walls, ornate trim, and custom windows, the cost to restore it to its previous condition can be far higher than rebuilding a newer home with off‑the‑shelf materials.

That is why some companies now carve out entire categories of older structures from their books. One report describes how a three‑unit, 1904 building that had survived two major earthquakes and was in good shape, according to the owner identified as Rich, still lost coverage when a carrier decided to exclude multi‑unit homes built before 1925. That kind of blanket cutoff shows how age itself can become a disqualifier, regardless of how carefully you maintain the property.

Foundations, structure, and the “silent deal‑breakers”

When you think about insurance red flags, you might picture a sagging roof or outdated wiring, but underwriters often start even lower, with the foundation and structure. Cracks, settling, and moisture problems are not just cosmetic, they signal potential instability that can turn a minor event into a major loss. Guidance aimed at older properties in Canada notes that foundation and structure issues are often “silent deal‑breakers,” because they are expensive to correct and hard to fully evaluate from the outside.

Inspectors working for carriers are trained to look for sloping floors, sticking doors, and visible movement in walls as signs of structural stress. A separate checklist of what insurers focus on highlights signs of settling as key risk indicators, right alongside plumbing and other systems. If your older home sits on a stone or brick foundation, or you have visible bowing or long horizontal cracks, you can expect questions, repair demands, or even a non‑renewal notice unless you can show recent professional evaluations and fixes.

Roofs, plumbing, and the obsession with system age

Few features trigger more scrutiny on an older home than the roof and plumbing, because they are directly tied to the most common and costly claims: water damage and interior destruction. Inspections that explain why some owners fail point out that your roof’s age matters especially if it is older than the carrier’s cutoff, because shingles and underlayment lose their ability to shed water long before they fall apart visibly. Once a roof crosses that line, some companies will only offer limited coverage or will require replacement as a condition of keeping the policy.

The stakes are clear in Florida, where one report notes that Progressive Insurance is shedding roughly 56,000 policies on homes with roofs older than 15 years, leaving many owners scrambling for alternatives. Inside the house, aging pipes and fixtures raise similar alarms, which is why guidance on home age flags plumbing as a critical system that needs to be updated before problems arise. If your supply lines are original galvanized steel or your drains are cast iron from the 1950s, insurers will often treat your home as a higher‑risk property until you can document modern replacements.

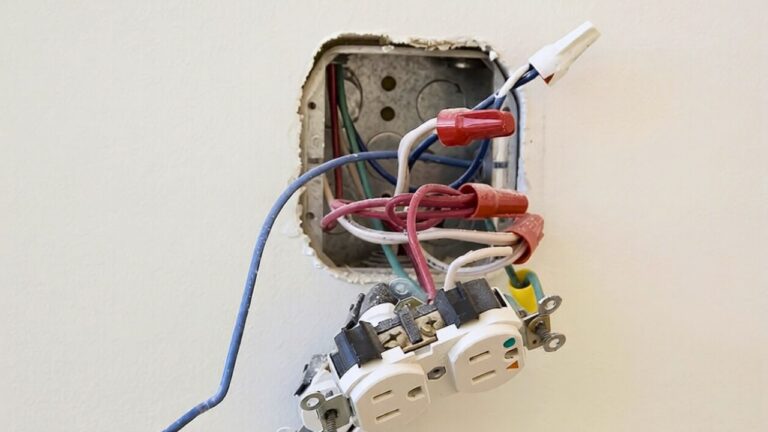

Electrical red flags, from aluminum wiring to DIY fixes

Electrical systems are another pressure point where older homes routinely trip alarms. Carriers are particularly wary of mid‑century properties that still rely on Aluminum Wiring, which was common in homes built in the late 1960s to mid‑1970s and is associated with a higher fire risk if not properly maintained. If your panel still feeds aluminum branch circuits without approved connectors or upgrades, you may find that only a handful of specialty carriers will write a policy, often at a steep premium.

Insurers are also increasingly skeptical of undocumented electrical work, especially in older houses that have seen decades of weekend projects. Reporting on interior risk factors notes that insurers are quietly cracking down on interior red flags, including makeshift wiring, overloaded outlets, and visible extension‑cord solutions that suggest the system is undersized. When you layer in guidance that critical systems like electrical and plumbing need proper documentation if you upgrade them yourself, the message is clear: in an older home, casual DIY work can turn into a coverage headache if you cannot prove it was done to code.

Inspections, clutter, and what insurers now look for

Because older homes carry more unknowns, carriers are leaning harder on inspections to decide whether to write or renew a policy. In storm‑prone regions, inspectors are instructed to focus on what insurance companies are looking for, including roof condition, drainage, and signs of water intrusion around the home, as outlined in guidance on rising insurance costs in areas like The Dallas and Fort Worth metroplex. For an older property, that means every patch, stain, and crack is interpreted through the lens of potential future claims.

Even your yard can become a liability trigger. Advice on policy cancellations explains why insurance companies are dropping coverage over backyard clutter, treating general signs of deferred upkeep as evidence that other, less visible maintenance is also being ignored. Another inspection guide singles out dilapidated outbuildings as a reason owners fail, because an old barn or unstable shed is a liability even if you rarely use it. For older homes, where detached garages and aging sheds are common, those details can be the difference between a clean inspection and a cancellation notice.

Historic character versus modern building codes

If your home is not just old but historically significant, the insurance puzzle gets even more complicated. Guidance on older and historical properties stresses that understanding the difference between standard and specialized coverage is essential, because restoring original features after a loss can cost far more than replacing them with modern equivalents. Ornate millwork, custom masonry, and period‑correct windows are expensive to replicate, and not every policy is designed to pay for that level of restoration.

At the same time, many historic homes do not meet current safety codes, which is exactly the kind of gap that makes insurers nervous. Overviews of home insurance for explain that carriers worry about outdated materials and systems that do not align with modern standards, from knob‑and‑tube wiring to narrow staircases and lack of egress windows. Another breakdown of why older homes notes that these properties often require specialized policies or endorsements to bridge the gap between historic character and current building codes. If you want both preservation and robust coverage, you have to be deliberate about the policy you choose.

Documentation, proof, and the burden on owners

As carriers tighten their standards, the burden of proof is shifting more squarely onto you as the homeowner, especially if your property is older. Even when you have invested in upgrades, you may find that your insurer will not take your word for it. One homeowner described how, after closing on a house, the company required them to provide specific documentation to prove age of the roof, with the understanding that, if requested, they would have to supply one of several listed records to Farmers or a Farmers Agent. Without that paper trail, the system defaults to assuming the worst‑case scenario for age and condition.

The same dynamic applies to DIY work on older homes. Reporting on coverage headaches warns that some of the most consequential projects involve critical systems like plumbing and roofs, and that failing to document them can undermine your ability to prove the home is a lower risk. In practice, that means keeping permits, contractor invoices, inspection reports, and photos for every major upgrade. In an older house, where the default assumption is that systems are original until proven otherwise, good records are often the only way to move your home out of the high‑risk bucket.

How you can keep an older home insurable

Despite the tougher climate, you are not powerless if you own an aging property. The first step is to see your home through an underwriter’s eyes and tackle the issues that move the needle most. Guidance aimed at older properties in Canada explains what actually moves with insurers, from addressing foundation and structural concerns to upgrading key systems, and notes that some carriers even give a small discount when you can show proactive work. Pair that with a pre‑emptive inspection focused on the same elements carriers care about, such as roof condition, drainage, and signs of settling, as outlined in what insurance companies for, and you can often fix problems before they show up on an insurer’s report.

It also pays to clean up the easy red flags that signal neglect, especially on older lots that have accumulated sheds, scrap, and half‑finished projects over the years. Advice on policy cancellations ties general signs of to a higher chance of being dropped, while inspection guidance warns that dilapidated outbuildings can sink an otherwise solid property. In a market where carriers are increasingly selective, especially with older homes, the owners who stay ahead of these red flags, document their upgrades, and align their maintenance with what underwriters actually care about will be the ones who keep their coverage, even as others struggle to find a company willing to say yes.

Like Fix It Homestead’s content? Be sure to follow us.

Here’s more from us:

- I made Joanna Gaines’s Friendsgiving casserole and here is what I would keep

- Pump Shotguns That Jam the Moment You Actually Need Them

- The First 5 Things Guests Notice About Your Living Room at Christmas

- What Caliber Works Best for Groundhogs, Armadillos, and Other Digging Pests?

- Rifles worth keeping by the back door on any rural property

*This article was developed with AI-powered tools and has been carefully reviewed by our editors.